Economists, politicians and Kiwi are wringing their hands over the cost of living in 2023, with inflation at a reportedly 32 year high at 7.2 per cent.

Rents are at an all time high and the Official Cash Rate (OCR) has once again been increased, so for those saving to buy a home and more, it feels like they can't catch a break, even with falling house prices and low unemployment.

So how bad, or good, are current conditions compared with decades past?

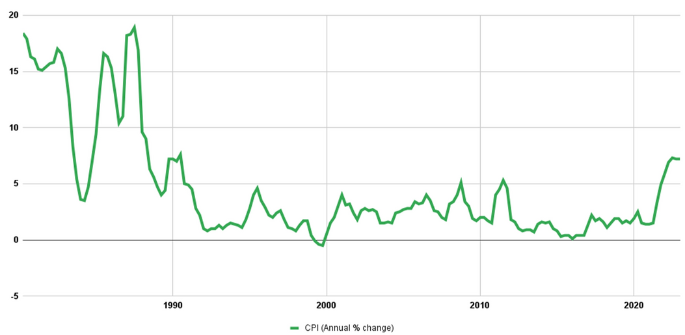

Consumer Price Index (CPI) (Annual per cent change)

Source: Stats NZ.

Chart Summary: The Consumers Price Index (CPI) measures changes to the prices of the consumer items New Zealand households buy, and provides a measure of household inflation.

These double-figure inflation rates in the 1980s were matched by a similar growth in incomes, says Infometrics chief forecaster, Gareth Kiernan, author of the Housing Update 2022 report which looked at relevant data from the past 70 years.

While current wages aren't increasing by double figures as they were in the 1980s, wages are strong at the moment, the highest percentages and the fastest growth in the past 30 years, says Gareth. There's been a 7.4 per cent increase in average hourly earnings for the year to December 2022 up from a 3.8 per cent increase in 2021, according to Stats NZ. He's expecting to see above-average wage inflation for the next 12 to 18 months, at around 3.5 per cent to 4 per cent.

At the same time, current inflation is right across the economy, food, fuel, household utilities and services. The CPI inflation rate of 7.2 per cent hasn't been this high since 1990, says Gareth. Between 1973 and 1990, inflation was running at 13 per cent to 14 per cent per annum.

'We're not at critical levels, just higher than it's been for a generation,” says Gareth.

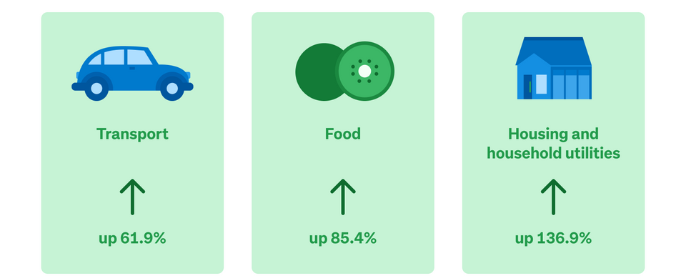

So, how much have prices increased?

In the last 23 years:

Figures from Stats NZ Consumer Price Index Outputs team.

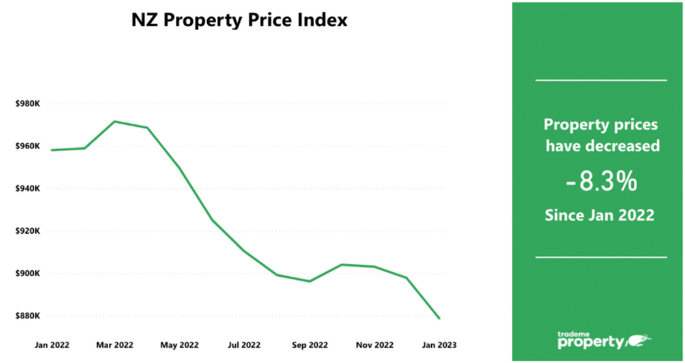

House inflation going in a different direction

While most consumer products are rising in price, Trade Me Property Price Index's national average asking price for a home fell by 8 per cent year-on-year in January 2023 to $879,800, the largest drop Trade Me has ever seen. In January 2022, by comparison, the national average asking price skyrocketed 25 per cent year on year, says Trade Me Property Sales director Gavin Lloyd.

Another piece of good news for first home buyers feeling held back by the high cost of living is that affordable homes around the country, likely to appeal to first home buyers are those dropping in price the most, according to interest.co.nz's Home Loan Affordabilty Report.

Prices dropped substantially in most regions of the country in January, according to REINZ, for instance in the Bay of Plenty, the selling price of the most affordable homes declined by 13.9 per cent from $692,000 in December to $596,000 in January 2023.

Housing is becoming more affordable as prices drop across the country.

But it's not all good news. Sense Partners' economist Shamubeel Eaqub says compared to the peak of the housing market things have gotten better on the deposit front but servicing the mortgage has become more expensive.

'The difference between now and the 1980s and 1990s is you could save a house deposit within 10 years of working and you could pay it off in 10 years if you were putting one third of your income into the mortgage,” he says.

Now it could take you decades to save the deposit if you're on a normal salary, he says, with people spending up to 40 per cent of their income on rent.

'The goal posts keep moving,” argues First Home Buyers' Club director, Lesley Harris. First home buyers are renters, and on top of that they have the cost of living to contend with, Auckland rents currently over a third of people's incomes, she says.

And those 20 per cent deposits are hard to get to when you're buying a million dollar house. 'When I bought my first house in the 1990s I could get 10 per cent lending, which is very hard now. There was a lot more 5 per cent lending in the 1990s but interest rates were higher then,” says Lesley.

Wages may be rising but house prices have risen by more in recent years, she says. The average asking price in Auckland for a home is $1,116,850 according to Trade Me, compared with December 2017 figures of $941,850. Peoples wages haven't gone up by that much, she says.

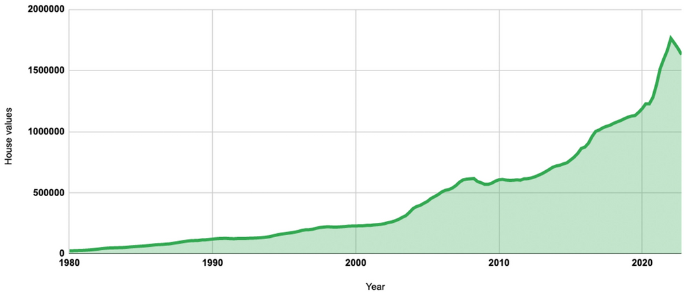

Value of housing stock over time

Source: CoreLogic. The data is compiled by CoreLogic and published by the Reserve Bank.

Easier to become a homeowner now than it used to be, says CoreLogic

CoreLogic chief property economist Kelvin Davidson believes it's easier to buy a home now than in the 1980s because credit is more widely accessible now than it was in the 1970s and 1980s when you needed to show an established savings record.

'You couldn't just go to a lender, you had to talk to the bank manager, there were no online applications going on,” says Kelvin.

For home buyers struggling with cost of living challenges, there's more assistance for first home buyers, says Jarrod Kirkland, General Manager of Mortgage Lab.

'What's changed from years ago is there's assistance for first home buyers with partners like Kāinga Ora,” he says.

When it comes to cost of living, the difference between now and a few years ago - it's harder to buy because you're paying more for the house but on the other hand it's easier to get finance, he adds.

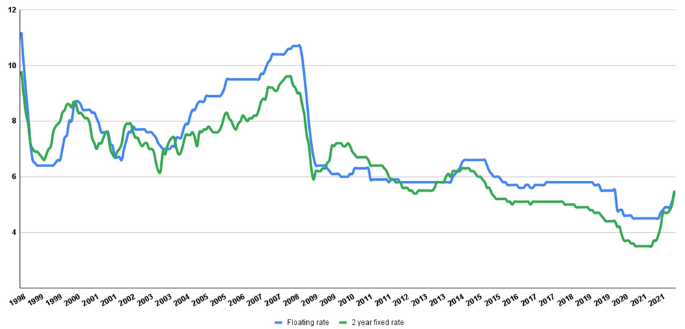

To homeowners dreading mortgage rates potentially increasing to 7 per cent, seasoned mortgage adviser Geoff Bawden reminds Kiwis that not that long ago the average interest rate was 7 per cent, and it was used as a barometer by mortgage advisers.

Banks Mortgage rates – Floating and 2 year fixed

Source: RBNZ

'A whole range of people think that a 3 per cent mortgage rate is normal but it's not sustainable,” he says. And it's not that people weren't tested to pay those higher rates but they're just not accustomed to paying those rates.

2 comments

Rents.

Posted on 09-03-2023 15:49 | By morepork

People having to pay 40% of their income so they can rent reasonable accommodation is outrageous. Landlords need a return on their investment, but the constraints on them have made many simply withdraw property from the rental market and just hold it for capital gain. So, we have people being squeezed for rent while suitable property stands empty. This is a no-win game for all concerned. Maybe we need to certify fair Landlords and good tenants and see that rent is no more than 30% for these people. Landlords who are profiteering should be penalized (fine them into a fund that helps lower income people get a roof:(bonds etc... ), and tenants who destroy or damage property have to live in tents/caravans, until they make full reparations. Perhaps we use temporary accommodation like transit camps or prefab buildings if there are children involved. No taxpayer-funded motels/hotels; what they DESERVE.

Hopeless?

Posted on 27-03-2023 16:13 | By Jason_88

I'll be honest, I've all but given up on ever owning a home in New Zealand. Rent prices are absurd - mine skyrocketed in March following the yearly review - but...what other choice do we have? How am I meant to live + save for a deposit + pay rent and and and... As Jarrod Kirkland highlighted, there are *a lot* of local providers offer low deposit options now. I think I saw Unity was the latest to partner up with Kainga Ora this year (can confirm: https://unitymoney.co.nz/get-a-loan/first-home-loan/ ) but with interest rates set to skyrocket I'm not sure if, even if I got my foot in the door, I'd be able to afford it. We're approaching a place where getting a deposit together is no longer half the battle but the start of the war...

Leave a Comment

You must be logged in to make a comment.